Decree 70 and Vietnam’s E-Invoice Reform: Avoiding Common Errors in Invoice Corrections and Tax Declarations

Vietnam’s e-invoice framework continues to evolve, with Decree 70/2025/ND-CP (“Decree 70”) introducing significant clarification around the treatment of incorrect e-invoices, invoice adjustments, replacement invoices, and the timing of associated tax declarations. While the decree took effect from 1 June 2025, many businesses continue to face practical difficulties in applying the new rules consistently in day-to-day operations.

Despite the clarifications in Decree 70, many enterprises continue to encounter practical difficulties when determining whether an incorrect e-invoice should be adjusted or replaced, and more critically, which tax period the correction should be declared in. Misapplication remains common and can create unnecessary VAT risks, reporting inconsistencies, and future tax audit exposure.

Understanding the distinction between issuance errors and post-transaction commercial adjustments is now critical for ensuring compliant invoice treatment under Vietnam’s evolving electronic invoicing regime. This article outlines the key principles businesses should understand when handling incorrect e-invoices under Decree 70, together with the practical implications for tax reporting and financial compliance.

Handling incorrect e-invoices – (Decree 70)

|

Step |

Category |

Applied to |

Required action |

Key requirement |

|

Step 1 – Identify the type of error |

(a) Minor errors (no impact on value) |

– Incorrect buyer name/address – Other details correct (including tax code and amounts) |

– Notify buyer |

No new invoice required. |

|

(b) Material errors (impact key information or value) |

– Incorrect tax code – Incorrect amount/tax/tax rate – Incorrect goods/services – Goods not meeting specifications or quality |

Proceed to Step 2 |

|

|

|

Step 2 – Choose the appropriate method |

Option 1 – Adjustment invoice |

o To be used: When the original invoice remains valid, but certain details need to be adjusted. o Typical cases: – Changes in quantity or unit price. – Changes in VAT rate or tax amount. – Errors in invoice details (e.g. amount, description, tax). – Sales returns (partial or full) (mandatory use). – Post-sale discounts / commercial rebates (mandatory use). |

|

Must clearly state:

Reflect the adjustment using positive (+) or negative (-) values as appropriate |

|

Option 2 – Replacement invoice |

o To be used: When the original invoice is incorrect and needs to be cancelled and fully replaced. o Typical cases:

|

|

Must clearly state: |

Notes:

• For each incorrect invoice, the seller is to apply only one method (either adjustment or replacement).

– Once a method is selected for the correction, it should be applied consistently.

– Subsequent corrections (if any) should continue based on the adjusted/replaced invoice, and to not switch methods arbitrarily.

• The handling of adjustment invoices: instead of writing “reduction,” when making a reduction adjustment, the seller now writes a negative sign (-) reflecting the actual amount. This change aims to standardize electronic data, enabling the tax authority’s system to automatically identify, reconcile, and accurately calculate revenue and VAT figures, thereby reducing errors compared to the previous manual reconciliation method.

Required Documentation

Before issuing an adjustment or replacement invoice, the supporting documentation requirements depend on the type of buyer. Where the buyer is an individual, the seller is required to notify the buyer of the error, either directly or through a public announcement (for example, on the seller’s website, if any).

For buyers that are enterprises, organizations, or business households, the seller and the buyer must prepare a written agreement or record clearly stating the nature of the error prior to issuing the corrective invoice. Such documentation must be retained by the seller and presented upon request by the tax authorities.

Invoice Issuance Process

The issuance process for adjustment or replacement invoices is as follows:

- The seller applies a digital signature.

- For e-invoices with tax authority code: the invoice must be submitted to the tax authority for code issuance before being sent to the buyer.

- For e-invoices without code: the invoice is sent directly to the buyer.

Multiple Incorrect Invoices

Where multiple incorrect invoices are issued to the same customer within the same month and involve similar errors, the seller is allowed to issue a single adjustment invoice or a single replacement invoice instead of correcting each invoice individually.

In these cases, the seller must attach a detailed list of the affected invoices in accordance with Form No. 01/BK-ĐCTT issued together with the relevant regulations.

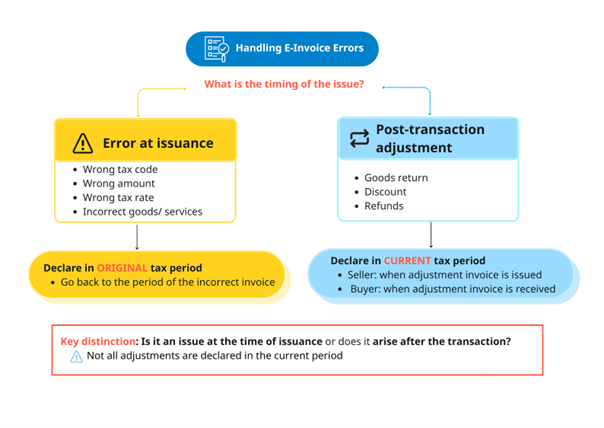

Tax Declaration Timing

The tax declaration treatment depends on the nature of the issue, not the type of invoice.

• Errors at issuance

→ Declare in the original tax period

• Post-transaction adjustments

→ Declare in the current period

(Seller: upon issuance; Buyer: upon receipt)

Key principle:

The distinction is whether the issue existed at issuance or arose after the transaction.

Practical Takeaways

To ensure compliant and consistent treatment, businesses should focus on the following:

- Correctly identify the nature of the issue (error vs. post-transaction adjustment)

- Apply the appropriate correction method (adjustment or replacement)

- Ensure the adjustment is accurately reflected (including +/- values where applicable)

- Declare in the correct tax period (original period vs. current period)

Decree 70/2025/ND-CP effectively resolves long-standing uncertainties regarding invoice corrections and tax declaration timing. By proactively adapting to Decree 70, businesses can standardize their financial data, minimize tax risks, and enhance corporate transparency.

For any further questions or assistance, please reach out to us at vietnam@alitium.com

********

This article is intended to provide an overview of recent updates and announcements. While it aims to present useful insights, it is important to note that the content shared here should not be considered as formal legal, tax or financial advice. For specific guidance on tax obligations or legal matters related to your business, we strongly recommend consulting with a qualified professional, such as a tax advisor or legal expert or directly reach out to us.