Vietnam Personal Income Tax (PIT) Compliance for Employers

For many employers, Personal Income Tax (PIT) compliance appears relatively straightforward. Monthly payroll is processed, tax is withheld, declarations are lodged and the annual PIT finalisation is completed. In practice, however, many of the most significant PIT exposures arise not from complex legislation, but from routine payroll processes, incorrect assumptions and small compliance errors that accumulate over time.

As Vietnam’s tax administration becomes increasingly digitalised and the tax authorities continue to strengthen their data matching and analytics capabilities, these issues are becoming easier to identify during tax inspections and annual reconciliations. At the same time, several legislative changes introduced during 2026 require employers to revisit established payroll procedures and reporting practices.

Drawing on Alitium’s experience advising businesses across a wide range of industries, this article highlights six of the most common PIT compliance issues we continue to encounter and the practical steps organisations can take to reduce unnecessary tax risk.

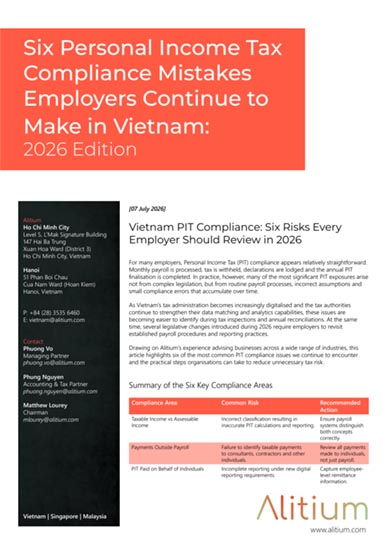

Summary of the Six Key Compliance Areas

|

Compliance Area |

Common Risk |

Recommended Action |

|

Taxable Income vs Assessable Income |

Incorrect classification resulting in inaccurate PIT calculations and reporting. |

Ensure payroll systems distinguish both concepts correctly. |

|

Payments Outside Payroll |

Failure to identify taxable payments to consultants, contractors and other individuals. |

Review all payments made to individuals, not just payroll. |

|

PIT Paid on Behalf of Individuals |

Incomplete reporting under new digital reporting requirements. |

Capture employee-level remittance information. |

|

Form 08 Commitments |

Incorrect acceptance of ineligible declarations. |

Verify eligibility and retain supporting documentation. |

|

PIT Finalisation |

Missing annual filings or reconciliation differences. |

Reconcile periodic declarations before annual filing. |

|

2026 Regulatory Updates |

Failure to adopt new filing timelines. |

Update compliance calendars and review historical filings regularly. |

1. Taxable Income vs Assessable Income: Getting the Tax Base Right

One of the most common causes of PIT reporting errors is confusion between Taxable Income and Assessable Income. Although the distinction appears technical, using the terms interchangeably can result in inaccurate declarations, validation errors and unnecessary compliance risk.

Under the Personal Income Tax Law 2025, Taxable Income represents income subject to PIT before statutory deductions. Assessable Income is the amount remaining after compulsory insurance contributions, personal and dependent deductions and other allowable deductions. PIT is calculated on the Assessable Income. As official declaration forms require both figures separately, payroll systems should clearly distinguish the two concepts and reconcile them before lodgement.

2. Looking Beyond Payroll

Many businesses focus exclusively on monthly payroll when considering PIT obligations. However, payments to freelancers, consultants, directors and individuals engaged under service agreements may also attract withholding obligations.

Likewise, the tax treatment of a payment for Corporate Income Tax purposes does not determine its PIT treatment. A payment may be non-deductible for CIT yet still require PIT withholding, declaration and remittance. Periodic reviews of all payments made to individuals are therefore an important component of an effective compliance framework.

3. New Reporting Requirements for Employer-Paid PIT

Article 12 of the Law on Tax Administration 2025 expands the information employers must provide when remitting PIT on behalf of individuals, including the employee’s Tax Identification Number, full name, tax withheld and tax remitted.

While implementation guidance is still evolving, businesses should review payroll and payment processes to ensure the required information can be produced accurately and consistently as implementation guidance continues to evolve.

4. Form 08: A Useful Relief or a Compliance Trap?

Form 08 can simplify payroll administration by allowing eligible individuals to request temporary non-withholding of PIT. However, employers should not accept these commitments without first ensuring employees understand the eligibility conditions.

Maintaining appropriate supporting documentation will assist in demonstrating that the employer acted reasonably should the declaration later prove incorrect.

5. Annual PIT Finalisation: The Ultimate Compliance Test

Annual PIT finalisation should be treated as a comprehensive reconciliation exercise rather than simply another filing obligation. Periodic declarations, payroll records and annual totals should reconcile before submission to minimise validation errors, rejected filings and potential penalties.

A disciplined reconciliation before submission can significantly reduce rejected filings, additional compliance work and potential administrative penalties.

6. New Filing Timelines, New Compliance Risks

The 2026 reforms introduce important procedural changes, including quarterly PIT declarations as the standard filing frequency and a reduction in the amendment period for historical returns from ten years to five years, and provide an opportunity for organisations to revisit their internal compliance framework.

Rather than waiting until year-end or a tax inspection, businesses should incorporate regular payroll reviews into their governance processes so potential issues are identified and addressed early.

Conclusion

Strong PIT compliance is no longer measured solely by whether returns are lodged on time. It is increasingly judged by the quality of payroll governance, the accuracy of data and an organisation’s ability to demonstrate consistent compliance across all aspects of its employment arrangements.

For many organisations, a periodic payroll and PIT health check is one of the most effective ways to identify issues before they become costly during a tax inspection.

At Alitium, we help employers move beyond compliance towards confidence. Through payroll compliance reviews, PIT health checks, annual finalisation support and practical advice on complex employer obligations, we assist organisations in building payroll processes that remain accurate, efficient and resilient as Vietnam’s regulatory environment continues to evolve.

For any further questions or assistance, please reach out to us at vietnam@alitium.com

********

This article is intended to provide an overview of recent updates and announcements. While it aims to present useful insights, it is important to note that the content shared here should not be considered as formal legal, tax or financial advice. For specific guidance on tax obligations or legal matters related to your business, we strongly recommend consulting with a qualified professional, such as a tax advisor or legal expert or directly reach out to us.