Invoicing Timing and the Updated Penalty Framework in Vietnam

Incorrect invoice issuance timing is one of the most common compliance issues faced by businesses in Vietnam. Most cases do not arise from deliberate non-compliance, but from confusion between payment timing, revenue recognition, and statutory invoicing requirements.

Recent regulatory updates under Decree 70/2025/ND-CP (amending Decree 123/2020/ND-CP) clarified invoice issuance principles and Decree 310/2025/ND-CP (amending Decree 125/2020/ND-CP), more importantly, restructured the administrative penalty framework. From 16 January 2026, penalties for late or incorrect invoicing will become clearer and potentially more severe.

This article summarizes the key invoicing timing rules and highlights the practical impact of the updated penalty regime for enterprises operating in Vietnam.

Key Legal Documents

- Decree 123/2020/ND-CP on invoices and supporting documents

- Decree 70/2025/ND-CP amending Decree 123/2020/ND-CP (effective from 1 June 2025)

- Decree 125/2020/ND-CP on administrative penalties for tax and invoice violations

- Decree 310/2025/ND-CP amending Decree 125/2020/ND-CP (effective from 16 January 2026)

Core Principles on Invoice Issuance Timing

Before reviewing industry-specific cases, it is useful to revisit two core principles that underpin Vietnam’s invoicing rules. These principles form the foundation that most businesses need to understand before considering detailed applications.

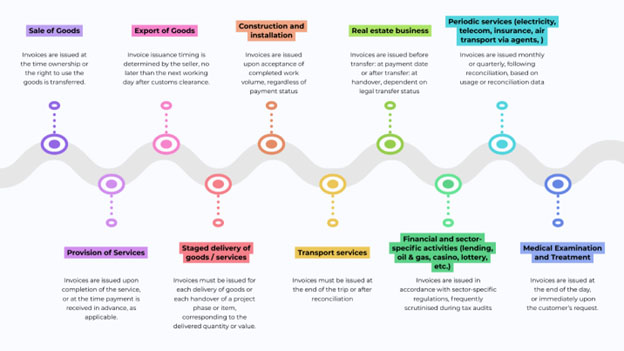

- Sale of Goods – Transfer of Ownership or Usage Rights

Invoices for the sale of goods must be issued at the time ownership or usage rights are transferred to the buyer, regardless of whether payment has been received.

For exported goods, including export processing activities, the seller may determine the invoice issuance date. However, the invoice must be issued no later than the next working day following customs clearance, in accordance with customs regulations.

- Provision of Services – Completion of Services

Invoices for services must be issued upon completion of the service, irrespective of payment status.

Where payment is collected in advance or during service performance, the invoice must generally be issued at the time of payment collection.

This rule does not apply to deposits or advances intended solely to secure contract performance for certain professional services, including accounting, auditing, tax and financial advisory, valuation, technical surveys and design, supervision consultancy, and construction investment project preparation.

For contracts performed in multiple stages or milestones, invoices must be issued for each completed portion, corresponding to the actual value of work performed.

Overview of Invoice Issuance Timing by Transaction Type

(This summary is prepared in accordance with Decree 123/2020/ND-CP and its amendments under Decree 70/2025/ND-CP.)

|

No. |

Transaction type |

Invoice issuance timing |

Practical notes |

|

1 |

Domestic sale of goods |

Upon transfer of ownership or usage rights to the buyer |

Payment timing is irrelevant |

|

2 |

Exported goods |

As determined by the seller |

No later than the next working day after customs clearance |

|

3 |

Provision of services |

Upon completion of the service |

If payment is received in advance, issue the invoice at the time of collection |

|

4 |

Staged delivery of goods or services |

Upon each delivery or handover |

Based on the actual value performed |

|

5 |

Insurance business activities |

When insurance revenue is recognized |

In line with industry practice |

|

6 |

Sale of pre-printed lottery tickets |

Periodically |

Not issued on a per-ticket basis |

|

7 |

Casino operations and prize-winning electronic games |

No later than one day after the revenue determination date |

Based on daily revenue reports |

|

8 |

Telecommunications services |

Based on periodic usage reconciliation |

Typically, monthly or quarterly |

|

9 |

Construction and installation activities |

Upon acceptance of completed work volume |

Regardless of payment status |

|

10 |

Real estate business |

Based on the payment schedule or transfer of rights |

Dependent on legal transfer status |

|

11 |

Air transport services |

Depend on how service is provided: – Via website or e-commerce systems: similar with service provision. – Not via website: Within five days from the issuance date of service documents – Through agents: upon completion of data reconciliation but no later than the 10th day of the following month. |

Not based on the flight date |

|

12 |

Crude oil exploration, extraction and processing |

When the official selling price is determined |

Independent of payment timing |

|

13 |

Sale of natural gas, associated gas and coalbed methane |

Upon determination of monthly delivered volume |

No later than the statutory monthly tax filing deadline |

|

14 |

Electricity sales |

After reconciliation of consumption volume |

On a monthly or quarterly basis |

|

15 |

Retail sale of petroleum products |

Upon completion of each sale transaction |

Issued per individual sale |

|

16 |

Lending activities |

In accordance with the interest collection schedule under the credit contract |

Issue immediately if interest is collected early or late |

|

17 |

Taxi passenger transport services |

At the end of each trip |

Per individual trip |

|

18 |

Medical examination and treatment services |

End of the day or immediately upon customer request |

Invoice Issuance Timing – Practical Decision Framework

The diagram translates statutory invoicing rules into a practical decision framework for common business transactions.

Common confusion: Advance payments vs. refundable deposits for services

A frequent area of confusion in practice relates to advance payments for services and refundable deposits intended to secure contract performance.

Generally, where payment is collected in advance or during service performance, an invoice must be issued at the time of collection.

However, this rule does not apply to refundable deposits or advances made solely to secure contract performance for certain professional services, such as accounting, auditing, tax and financial advisory, valuation, technical surveys and design, supervision consultancy, and construction investment project preparation.

In assessing the correct invoicing treatment, businesses should focus on the substance of the payment, including:

- Whether the amount is refundable.

- The nature of the service.

- Whether it represents consideration for services already performed or to be performed, and

- The contractual terms governing the payment.

Incorrect classification of deposits as service advances is a common cause of incorrect invoice timing and may expose businesses to administrative penalties under the updated regulations.

Administrative Penalties for Incorrect Invoice Timing

Penalties under the Current Framework

Under Decree 125/2020/ND-CP, issuing invoices at an incorrect time may result in:

- Warning, where no delay in tax obligations arises and mitigating factors apply.

- Monetary fines of VND 3 – 5 million, where incorrect timing does not delay tax payment.

- Monetary fines of VND 4 – 8 million, for other cases of incorrect invoice timing.

In practice, incorrect invoicing timing often triggers follow-up tax reviews, including reassessment of VAT declarations, late payment interest, and increased audit scrutiny.

Revised Penalty Framework Effective from 16 January 2026

Under Decree 310/2025/ND-CP, penalties for invoice violations are determined based on both the nature of the transaction and the number of violating invoices. Separate penalty thresholds apply to revenue-generating sales and to non-commercial or internal-use transactions, as summarized below:

Table 1 – Non-commercial / internal-use transactions

(Promotions, samples, gifts, internal consumption, benefits in kind, lending/borrowing of goods)

|

Number of violating invoices |

Incorrect timing (VND) |

No invoice issued (VND) |

|

1 |

Warning |

Warning |

|

2 to <10 |

0.5 – 1.5 million |

1 – 2 million |

|

10 to <50 |

2 – 5 million |

2 – 10 million |

|

50 to <100 |

5 -15 million |

10 – 30 million |

|

≥100 |

15 – 30 million |

30 – 50 million |

Table 2 – Revenue-generating sales of goods and services

|

Number of violating invoices |

Incorrect timing (VND) |

No invoice issued (VND) |

|

1 |

0.5 – 1.5 million |

1 – 2 million |

|

2 to <10 |

2 – 5 million |

2 – 10 million |

|

10 to <20 |

5 – 15 million |

10 – 30 million |

|

20 to <50 |

15 – 30 million |

30 – 50 million |

|

50 to <100 |

30 – 50 million |

60 – 80 million |

|

≥100 |

50 – 70 million |

60 – 80 million |

Key notes:

- Penalties apply to organizations; individuals are subject to 50% of the organizational fine.

- Multiple violations on the same day are subject to a single penalty at the highest applicable level.

- Decree 310/2025/ND-CP takes effect from 16 January 2026.

Practical Implications and Recommendations

The updated regulations reaffirm Vietnam’s approach of aligning invoice issuance with the economic substance and timing of transactions, while the revised penalty framework significantly strengthens enforcement through clearer classification and higher exposure.

Decree 310/2025/ND-CP introduces more structured and prescriptive rules on how penalties are determined, reducing interpretational flexibility in enforcement. It can be likened to a multi-step ladder: the more violations you commit (the greater the number of invoices involved), the higher the penalty “step,” rather than a single uniform penalty applying to all violations as in the Decree 125/2020/ND-CP.

In light of these changes, enterprises should consider:

- Reviewing invoicing workflows against delivery, acceptance, and service completion milestones.

- Ensuring consistency between contracts, acceptance records, payment schedules, and invoice issuance dates.

- Strengthening controls over advance payments, staged transactions, and non-commercial activities, and

- Proactively assessing compliance readiness ahead of the 2026 penalty regime to mitigate financial and reputational risks.

For any further questions or assistance, please reach out to us at vietnam@alitium.com

********

This article is intended to provide an overview of recent updates and announcements. While it aims to present useful insights, it is important to note that the content shared here should not be considered as formal legal, tax or financial advice. For specific guidance on tax obligations or legal matters related to your business, we strongly recommend consulting with a qualified professional, such as a tax advisor or legal expert or directly reach out to us.