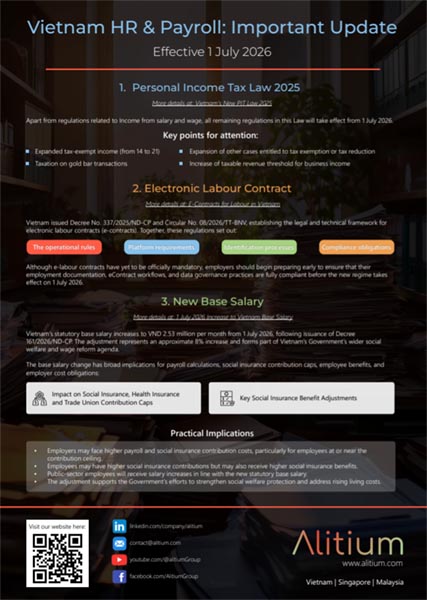

Changes in Vietnam to HR & Payroll Regulations from 1 July 2026

From 1 July 2026, several important regulatory changes will take effect, affecting how businesses manage employee remuneration, payroll administration, employment documentation and statutory obligations.

While many employers are aware that regulatory changes are on the horizon, fewer have assessed the practical implications for their organisation. Depending on workforce structure and existing HR processes, these developments may influence payroll costs, employee benefits, tax planning opportunities, and administrative requirements.

For foreign-invested enterprises (FIEs), multinational organisations, and businesses employing both local and expatriate staff in Vietnam, early preparation will be key to ensuring compliance and minimising operational disruption.

The key changes include:

- New provisions under the Personal Income Tax Law 2025

- The introduction of a legal and technical framework for electronic labour contracts (e-contracts)

- An approximately 8% increase in Vietnam’s statutory base salary to VND 2.53 million per month

Below, we examine what is changing, the potential impact on employers, and the practical steps businesses should consider before the new rules take effect.

1. Personal Income Tax Law 2025: Is Your Compensation Structure Still Optimised?

New PIT Rules: More Exemptions, New Obligations

The Personal Income Tax (PIT) Law 2025 introduces several significant changes to Vietnam’s tax framework. While regulations relating to salary and wage income will take effect under a separate timeline, the remaining provisions of the law will become effective from 1 July 2026.

For employers, these changes are worth noting as they may affect employee benefits, contractor arrangements, and broader workforce planning decisions.

Expanded tax-exempt income categories

The number of tax-exempt income categories increases from 14 to 21.

For employers, this creates an opportunity to review how employee compensation packages are structured. Certain benefits, allowances, or payments that may previously have been taxable could now fall within expanded exemption categories.

Businesses that review their compensation arrangements early may be able to improve tax efficiency while maintaining compliance.

Higher taxable revenue thresholds for business income

The new law also broadens the range of circumstances in which tax exemptions or tax reductions may apply.

In addition, the revenue threshold applicable to certain business income has been increased. Under the new framework, individuals conducting business activities with annual revenue of VND 500 million or less may no longer be subject to Personal Income Tax, significantly increasing the previous threshold.

While this change primarily affects household businesses, freelancers, independent contractors, and self-employed individuals, it may also be relevant for businesses that engage external consultants or service providers as part of their workforce model.

Businesses that utilise contractors, consultants, or project-based resources should consider reviewing these arrangements to understand whether the new rules may affect tax treatment or engagement structures.

New Rules for Certain Types of Income

The law also introduces new tax rules for income arising from gold bar transactions and updates the revenue thresholds applicable to certain business activities. While these changes may not affect every employer directly, they are part of a broader effort to modernise Vietnam’s tax framework and expand the range of income categories covered by the legislation.

Broader tax exemption and reduction cases

The law expands the categories of individuals and income types qualifying for PIT exemption or reduction. Review whether your employee mix benefits from any new categories.

What Employers Should Review

Businesses should assess whether their current remuneration structures remain appropriate under the revised framework, including:

- Expatriate remuneration packages

- Benefits-in-kind

- Housing and relocation allowances

- Executive compensation arrangements

- Cross-border mobility programmes

Businesses that review their compensation structures early may identify opportunities to improve tax efficiency while ensuring ongoing compliance with the new rules.

2. Electronic Labour Contracts: Prepare Before It Becomes Mandatory

Vietnam has issued Decree No. 337/2025/ND-CP and Circular No. 08/2026/TT-BNV, establishing the complete legal and technical framework for electronic labour contracts. E-contracts are not yet universally mandatory across the private sector, but the infrastructure and compliance requirements are live from 1 July 2026.

Why businesses should transition to e-contracts

- Legal equivalence: E-contracts carry the same legal weight as traditional paper contracts.

- Administrative efficiency: Contract data on the centralised platform can be shared directly for public services and administrative procedures, reducing time and cost.

- Enhanced security: Each contract receives a unique ID, preventing duplication or falsification. The platform maintains a full audit trail for 10 years after contract termination.

- Ease of access: Both parties can register accounts to look up, verify, and manage contract data through the national platform.

The signing process and digital signatures

E-contracts must be executed through specialised software supporting digital signatures and time-stamping. Both parties must use digital signatures. Employers are legally responsible for providing the necessary guidance, training, and means to support employees through this process. Authentication can be integrated via the National Electronic Identification System (VNeID) Level 2 or chip-based citizen ID cards.

Cost considerations

- Employers: Typically pay service fees to e-contract providers for creation, signing, and storage, as well as costs for their own digital signatures and time-stamping services.

- Employees: Are protected from unreasonable costs. The law stipulates that costs or risks arising from errors by the e-contract provider cannot be transferred to the employee unless otherwise agreed.

3. New Statutory Base Salary

Base Salary Rises to VND 2.53 million: Direct Impact on Payroll Costs

Under Decree 161/2026/ND-CP, Vietnam’s statutory base salary increases approximately 8% to VND 2.53 million per month from 1 July 2026. This is not a standalone adjustment, it flows directly into social insurance contribution caps, health insurance calculations, trade union contributions, and statutory benefit payouts.

|

What changes |

Business impact |

|

Social insurance contribution caps |

Caps recalculated upward: higher cost for employers and employees near the ceiling |

|

Health insurance contributions |

Adjusts in line with the new base salary |

|

Trade union contributions |

Employer obligations increase proportionally |

|

Social insurance benefit payouts |

Sick leave, maternity, and other benefits recalculated upward |

|

Public-sector salaries |

All public-sector staff receive salary increases tied to the new base rate |

What does that mean for payroll and budget implications?

For businesses with employees at or near contribution ceilings, the increase may result in higher payroll-related costs.

Employers should review:

- Payroll budgets

- Social Insurance projections

- Workforce cost forecasts

- Employee communication plans

Understanding the financial impact in advance will help organisations avoid unexpected cost increases and ensure accurate budgeting for the second half of 2026.

What Employers Should Do Before 1 July 2026

With multiple HR, payroll and tax changes taking effect from 1 July 2026, businesses should avoid reviewing each change in isolation.

The interaction between employee remuneration, payroll calculations, social insurance obligations and employment documentation means that changes in one area may have implications for another.

In preparation for the upcoming changes, employers should consider:

- Review Compensation and Benefits Structures: Reviewing employee compensation structures, allowances and benefits against the new Personal Income Tax framework.

- Evaluate E-Contract Readiness: Determine whether current systems, processes, and documentation can support compliant electronic labour contracts.

- Recalculate Payroll Costs: Update budgets and forecasts to reflect the new statutory base salary and revised contribution ceilings.

Businesses that begin reviewing these areas early are likely to be better positioned to manage compliance risks, avoid operational disruption and identify potential efficiencies within their HR and payroll functions.

How Alitium Can Help

Alitium supports businesses across Vietnam, Singapore, and Malaysia with HR advisory, payroll compliance, employment documentation, and workforce administration services.

If you would like to understand how these upcoming changes may affect your organisation, our team can assist with a practical review of your HR and payroll arrangements.

For any further questions or assistance, please reach out to us at vietnam@alitium.com

*********

This guide is intended as a general overview only and does not constitute legal or tax advice. Outcomes, procedures and requirements vary depending on specific circumstances, contractual structures, and regulatory interpretation. Investors should seek professional advice before relying on this information.