Global Minimum Tax in Vietnam: Impact on Tax Incentives and MNE Compliance

Vietnam has secured its position as an attractive investment destination partially attributable to Corporate Income Tax incentives such as tax holidays and preferential rates. However, with the introduction of the Global Minimum Tax (GMT) and recently the Decree No. 236/2025/NĐ-CP (Decree 236) on 29 August 29 2025, (instructions for the application of the Global Minimum Tax in Vietnam), many companies are now experiencing a difficult result: Their incentives may still exist, but their savings may not.

The Shift: From “Low Tax” to “Minimum Tax”

Under the GMT rules, multinational groups with consolidated revenue of EUR 750 million or more must achieve a minimum effective tax rate (ETR) of 15% in each jurisdiction.

Through Decree 236, Vietnam has implemented the Qualified Domestic Minimum Top-up Tax (QDMTT) to collect any shortfall where an in-scope group’s ETR in Vietnam falls below 15%.

This prevents other countries (e.g., the parent company’s country) from collecting the top-up tax under the Income Inclusion Rule (IIR) or the Undertaxed Payments Rule (UTPR).

For example:

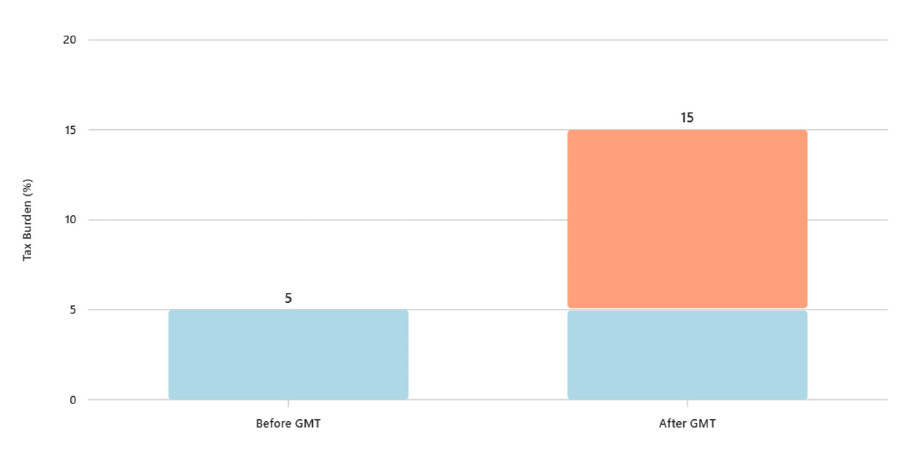

An IT company which enjoys CIT incentives in Vietnam may be impacted by GMT if their consolidated group revenue is above EUR 750 million:

• Before GMT, the incentive rate is 5%.

• After GMT, they will need to pay up to 15%, which means an additional 10% will arise.

Before GMT, a low tax rate created real and permanent savings, allowing profits to remain within the group. After GMT, a low tax rate only provides a temporary benefit, as the difference must be paid back as a top-up tax. The incentive loses its effect and no longer provides a meaningful tax advantage.

How businesses should approach Global Minimum Tax

Under Global Minimum Tax, tax exposure is no longer determined by statutory tax rates or preferential incentives stated in investment licenses. Instead, it is driven by the group’s Effective Tax Rate (ETR) calculated under GMT methodology. ETR reflects the proportion of tax actually borne compared with profit:

ETR = Total tax expense / GMT-adjusted profit

• Where ETR is below 15%, Vietnam will impose QDMTT top-up tax

• Where ETR is at or above 15%, no top-up tax arises

In practical terms, tax strategy now shifts from managing “incentive rates” to managing ETR outcomes.

Implications for Businesses

• Loss of incentive value: Tax holidays and reduced CIT rates may no longer reduce the global tax burden. Businesses may be impacted by this regulation:

o Preferential CIT rates (5%, 7%, 10%)

o Tax holidays

o High-tech or software incentives

o Industrial zone approvals

• Compliance complexity: MNEs must calculate effective tax rates under GMT and prepare for additional reporting obligations. Failure to comply with GMT may result in tax reassessments, penalties, or enforcement actions by tax authorities.

• Under GMT:

o Accounting profit is recalculated in accordance with OECD rules

o Tax expense is standardized for GMT purposes

• Strategic reassessment: Companies may need to reconsider investment structures, as location-based tax benefits diminish. Failure to optimize the investment structure may result in loss of competitive advantage and higher costs.

Investment plans aimed at optimizing tax incentives may need to be reconsidered, while on the other hand, plans based on other critical factors such as geopolitical advantages, labour costs, workforce availability, and supply chain benefits will still proceed.

What should each MNE group do?

• Assess exposure: Calculate your effective tax rate under GMT rules.

• Model scenarios: Understand how much of your current tax benefit could be clawed back.

• Engage in dialogue: Work with advisors and authorities to explore alternative support measures (e.g., labour, infrastructure support).

• Enhancing governance and data capabilities.

The era of tax-driven investment strategies is changing. Under GMT and Decree 236, Vietnam’s traditional tax incentives face diminishing returns for large MNEs.

Final Thoughts and Strategies

Vietnam has not withdrawn its tax incentives. However, the introduction of Global Minimum Tax has reshaped their practical value. Although incentives remain legally available, their financial benefit may be significantly reduced or fully neutralised.

Vietnam’s Decree 236 took effect on 15 October 2025, but is applicable from the 2024 tax year. This means Global Minimum Tax is has already impacted taxpayers 2024 position, even before formal enforcement began. For groups operating under preferential regimes in Vietnam, this is no longer a hypothetical issue, and remains a true commercial reality. The effective tax burden has already changed for many, whether or not it has been formally assessed.

For any further questions or assistance, please reach out to us at vietnam@alitium.com

********

This article is intended to provide an overview of recent updates and announcement. While it aims to present useful insights, it is important to note that the content shared here should not be considered as formal legal, tax or financial advice. For specific guidance on tax obligations or legal matters related to your business, we strongly recommend consulting with a qualified professional, such as a tax advisor or legal expert or directly reach out to us.