Geopolitical Resilience and Structural Advantage: Why Vietnam, Singapore and Malaysia Stand Out for Global Investors

Amid rising geopolitical uncertainty and shifting global supply chains, Southeast Asia is increasingly attracting international capital. This article examines how Vietnam, Singapore and Malaysia each play a distinct role in the regional investment ecosystem, from manufacturing scale to financial structuring and fiscal competitiveness, and why investors are increasingly structuring operations across these three markets.

Vietnam Adopts the Apostille Convention: Simplifying Cross-Border Document Authentication

Vietnam’s adoption of the Hague Apostille Convention, effective September 2026, will simplify the authentication of foreign public documents used in Vietnam. The new system replaces the traditional multi-step consular legalization process with a single Apostille certification. This reform is expected to reduce processing time, lower administrative costs, and streamline cross-border transactions for businesses operating internationally.

Transfer Pricing Inspections in Vietnam: High-Risk Indicators and Common Violations

Transfer pricing inspections have become a key focus of the Vietnamese tax authorities as multinational group structures and cross-border transactions become more common. Enterprises engaging in related-party transactions are required to comply with Vietnam’s transfer pricing regulations, including disclosure obligations and the preparation of supporting documentation under Decree 20/2025/ND-CP.

Vietnamese tax authorities increasingly apply risk-based screening methods to identify companies that may warrant closer examination. Certain financial patterns and transaction structures (such as persistent losses, significant related-party payments abroad, or unusually low profitability compared with industry peers) may trigger transfer pricing audits.

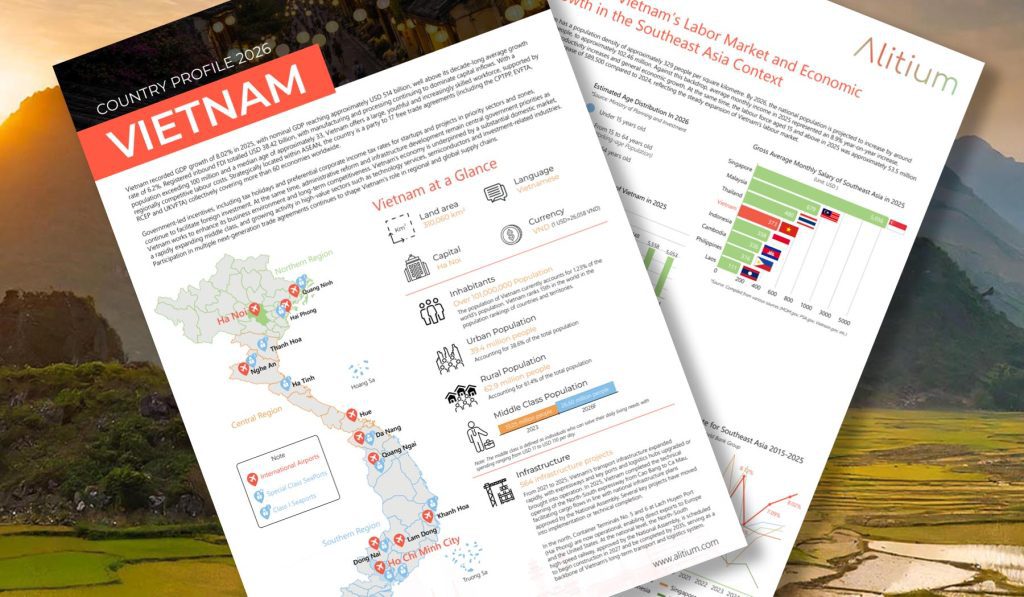

Vietnam Country Profile 2026

Alitium’s Vietnam Country Profile 2026 provides a comprehensive overview of Vietnam’s economic performance, foreign direct investment trends, trade profile, labour market, infrastructure development and growth outlook. Designed for foreign investors, corporates and advisors, the guide highlights Vietnam’s 8.02% GDP growth in 2025, USD 38.42 billion in registered FDI, expanding middle class, competitive workforce and strategic ASEAN positioning.

The guide supports businesses evaluating market entry, expansion or supply chain diversification into one of Southeast Asia’s fastest-growing economies.

Singapore Family Offices

Singapore has become the leading Asia-Pacific hub for Single-Family Offices, supported by robust regulation, political stability and attractive tax incentives under Sections 13O and 13U of the Income Tax Act.

This article provides a practical overview of how Single-Family Offices are structured and regulated in Singapore, the qualifying criteria for tax exemptions, and the compliance obligations families should expect. It also examines recent and proposed MAS developments, including changes to class exemption frameworks, ownership structures, and anti-money laundering requirements, offering guidance for ultra-high-net-worth families considering Singapore as their long-term wealth management base.

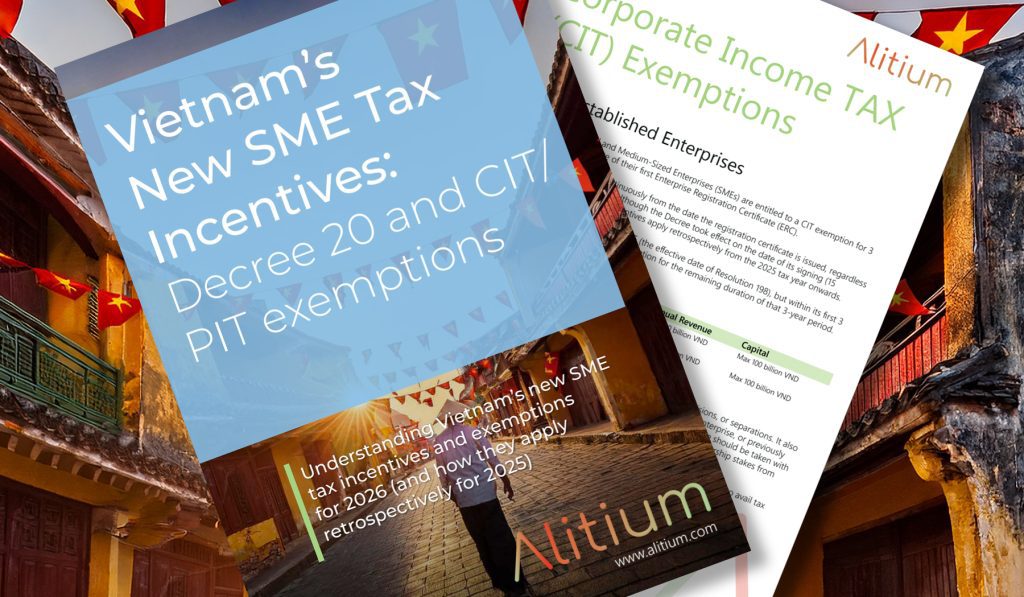

Vietnam’s New PIT & CIT Exemptions & Incentives

On 15 January 2026, the Government of Vietnam issued Decree No. 20/2026/ND-CP (Decree 20), introducing a comprehensive package of Corporate Income Tax (CIT) and Personal Income Tax (PIT) incentives aimed at accelerating private sector growth, innovation, and startup activity.

Decree 20 provides targeted tax exemptions and reductions for newly established SMEs, innovative startups, startup support organisations, investors, and experts and scientists, with several incentives applying retrospectively from the 2025 tax year. The framework is activity-based rather than size-based, placing emphasis on innovation, research and development, and genuine economic substance.

This guide explains how Decree 20 operates in practice, including eligibility criteria, exemption periods, exclusions, and common risk areas, offering practical insight for foreign-invested enterprises, founders, and investors operating in Vietnam’s evolving tax environment.

Singapore Company Incorporation in 2026

A practical yet comprehensive guide for organizations and businesses considering the establishment of a private limited company in Singapore – one of the world’s leading global business hubs. With a transparent legal framework, streamlined registration procedures, and attractive business support policies, Singapore has become an ideal destination for investors seeking to expand their operations in the Asia-Pacific region.

Vietnam’s Personal Income Tax Law 2025: Impact on Vietnamese Taxpayers in 2026

Vietnam’s Personal Income Tax Law 2025 marks a major reform to the country’s PIT framework, taking effect from 2026. Key changes include increased personal and dependent deductions, simplified progressive tax brackets, expanded tax exemptions, new taxable income categories and targeted incentives for high-tech personnel, startups and green economy activities. This article outlines the practical impacts for employees, individual taxpayers and businesses operating in Vietnam, and highlights compliance considerations ahead of implementation.

Vietnam Year-End 2025 Tax Compliance: Key CIT, PIT and VAT Requirements and Deadlines

Vietnam’s 2025 year-end tax finalisation is a transitional compliance year following major legislative changes to the Corporate Income Tax regime. This guide outlines key deadlines for Corporate Income Tax (CIT), Personal Income Tax (PIT) and VAT filings, required forms and submission requirements, penalty exposure and practical considerations for companies and income-paying organisations operating in Vietnam.

Vietnam’s New Corporate Income Tax Rules: Key Changes Under Decree 320

Decree 320/2025/ND-CP provides detailed guidance on Vietnam’s new Corporate Income Tax Law from December 2025. This article outlines key changes affecting taxable income, loss offsetting, real estate transfers, capital transfers, incentives, and compliance obligations for enterprises operating in Vietnam.